Published by Lookforzebras

Congratulations on embarking on your journey as a resident physician! This is an exciting time filled with opportunities for growth and learning. Amidst the challenges and demands of residency, it’s essential to lay the groundwork for your financial future. Financial planning might seem daunting, but with the right approach, you can set yourself up for long-term success and security.

This comprehensive guide is tailored specifically for resident physicians like yourself, offering straightforward advice, practical tips, and financial planning for medical residents to help you navigate the complexities of managing your finances during this pivotal stage of your career. Whether you’re just starting residency or nearing its completion, this guide will provide you with the knowledge and tools you need to make informed decisions about budgeting, saving, investing, and more.

By taking control of your finances early on and developing financial residency, you can build a solid foundation that will serve you well throughout your medical career and beyond. So, let’s dive in and explore the key principles of financial planning for resident physicians, empowering you to achieve your goals and aspirations with confidence.

Financial Planning for Medical Residents – What Are The Different Methods Of Budgeting and Financial Planning?

Budgeting and financial planning are crucial aspects of personal and business finance management. There are various methods and approaches to budgeting and financial planning, each suited to different needs, preferences, and circumstances. Here are some common methods:

Traditional Budgeting:

This involves estimating income and expenses over a specific period (usually monthly or annually) based on historical data or expected future income and expenses.

It typically involves categorizing expenses into fixed (e.g., rent, utilities) and variable (e.g., groceries, entertainment) and allocating funds accordingly.

Zero-Based Budgeting (ZBB):

In ZBB, every dollar of income is allocated to expenses, savings, or investments. This means that expenses must equal income, resulting in a balance of zero.

It requires reevaluating expenses regularly and justifying each expense, which can lead to better cost control and resource allocation.

Envelope System:

This method involves dividing cash into separate envelopes labeled with different expense categories (e.g., groceries, entertainment).

Once an envelope is empty, there is no more spending in that category until the next budget period. It helps control spending and prioritize expenses.

50/30/20 Budget Rule:

This rule suggests allocating 50% of income to needs (such as housing and utilities), 30% to wants (such as dining out and entertainment), and 20% to savings and debt repayment.

It offers a simple guideline for budgeting and ensures a balance between immediate needs, lifestyle choices, and financial goals.

Priority-Based Budgeting:

In this approach, expenses are ranked based on their importance or priority to the individual or household.

High-priority expenses, such as rent or loan payments, are funded first, followed by medium-priority expenses like groceries, and finally, lower-priority expenses like entertainment.

Incremental Budgeting:

This method involves making adjustments to the previous budget based on changes in income, expenses, or other financial factors.

It’s often used in businesses where budgets are adjusted incrementally from the previous period, rather than starting from scratch each time.

Pay Yourself First:

This method prioritizes savings by setting aside a portion of income for savings or investments before paying other expenses.

It ensures that saving for the future is given top priority, promoting long-term financial stability and wealth accumulation.

Proportional Budgeting:

In this approach, expenses are allocated as a percentage of income. For example, housing might be set at 30% of income, transportation at 15%, and so on.

It provides a flexible way to adjust expenses according to changes in income while maintaining a consistent saving strategy.

Different individuals and organizations may find certain methods more suitable depending on their financial goals, lifestyle, and preferences. It’s essential to choose a budgeting method that aligns with your needs and helps you achieve your financial objectives.

Financial Planning for Medical Residents – Medical Debt Overhang of Resident Doctors

Medical debt is a significant issue faced by many resident doctors in the United States. The combination of high tuition fees for medical school, living expenses during residency, and relatively low salaries during residency can result in substantial debt burdens for medical trainees.

Here are some key points regarding the medical debt overhang of resident doctors:

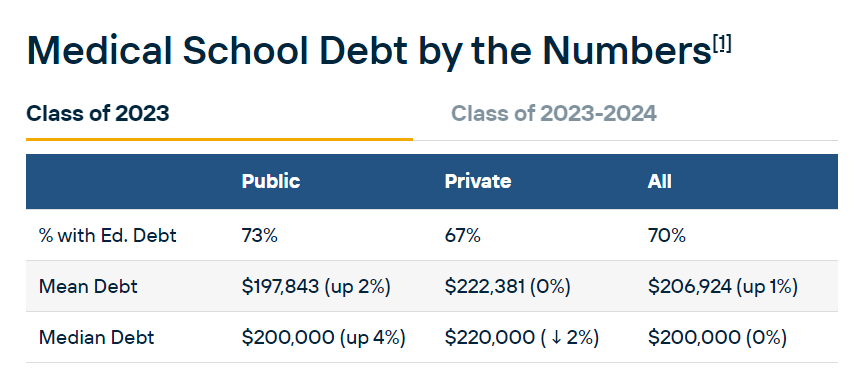

High Cost of Medical Education: Medical school tuition fees in the United States are among the highest in the world.

Source: Laurel Road.com

Limited Earning Potential During Residency:

Despite being highly educated professionals, resident doctors typically earn modest salaries during their training. The average salary for a resident physician in the United States ranges from about $50,000 to $60,000 per year, depending on specialty and location. This income may not be sufficient to cover living expenses and loan payments, especially for those with significant debt.

Accumulated Debt:

Many medical students graduate with substantial student loan debt, which continues to accumulate interest during residency. By the time they complete their training, some residents may owe hundreds of thousands of dollars in student loans.

Financial Stress and Burnout:

The burden of medical debt can contribute to financial stress and impact the mental well-being of resident doctors. Financial concerns, along with the demanding nature of residency training, can increase the risk of burnout among medical trainees.

Limited Repayment Options:

While there are loan repayment and forgiveness programs available for healthcare professionals, such as Public Service Loan Forgiveness (PSLF) and income-driven repayment plans, navigating these programs can be complex, and not all residents may qualify. Additionally, some specialty choices may not be eligible for certain repayment programs.

Potential Impact on Career Choices:

The need to repay medical debt may influence career decisions for resident doctors. Some may feel pressured to pursue higher-paying specialties or practice in underserved areas to qualify for loan forgiveness programs, rather than following their personal interests or pursuing careers in areas of need.

Addressing the medical debt overhang of resident doctors requires a multi-faceted approach, including policies to reduce the cost of medical education, increase residency salaries, expand loan forgiveness programs, and provide financial education and support for medical trainees. By alleviating the financial burden on resident doctors, we can help ensure that they are better able to focus on their training and provide high-quality care to patients.

Financial Planning for Residents -Early Financial Considerations During Residency

During residency, your financial situation might be tight due to lower income compared to when you become an attending physician. Living like a resident is an important factor you must consider. However, there are several important financial considerations you should address during this time to set yourself up for future financial success:

Budgeting:

Create a residency budget spreadsheet to track your expenses and ensure you’re living within your means. Identify essential expenses such as rent, utilities, groceries, and transportation, and allocate funds accordingly. According to a Medscape survey, the average resident’s salary was $67,400 per annum. Start your budgeting exercise early in your career using an app, a spreadsheet, or one of the methods described in the preceding section. There are always unexpected expenses that creep up but budgeting enforces financial discipline.

Emergency Fund:

Start building an emergency fund to cover unexpected expenses like medical emergencies, car repairs, or job loss. Aim for at least three to six months’ worth of living expenses in a high-yield savings account.

Student Loans:

If you have student loans, consider enrolling in an income-driven repayment plan to reduce monthly payments during residency. Explore options for loan deferment or forbearance if needed, but be mindful of interest accruing during these periods.

Retirement Savings:

Contribute to your employer-sponsored retirement plan, such as a 401(k) or 403(b), especially if your employer offers a match. Even small amounts saved regularly can grow significantly over time due to compounding interest and help you with your residency funding solutions.

Insurance:

Ensure you have adequate health insurance coverage, either through your employer or a private plan. Consider disability insurance to protect your income in case of injury or illness preventing you from working. Insurance includes both life insurance and disability insurance payments. Insurance can help to preserve your assets when you are facing a legal suit.

Side Income:

Explore opportunities for supplemental income or how to make extra money during residency, such as moonlighting, freelance work, or tutoring, to boost your cash flow. Be mindful of any restrictions imposed by your residency program. Medical wealth management is important in this phase,

Housing:

Look for affordable housing options, such as shared apartments or renting a room, to minimize housing expenses. Consider proximity to your workplace to reduce commuting costs. This will also help you in your medical financial planning exercise,

Professional Development:

Invest in continuing education and networking opportunities that can enhance your skills and advance your career prospects. Attend conferences, workshops, or online courses relevant to your specialty.

Tax Planning:

Familiarize yourself with tax deductions and credits available to residents, such as the student loan interest deduction and the Lifetime Learning Credit. Consider consulting a tax professional for personalized advice.

Financial Literacy:

Educate yourself about personal finance topics, including investing, saving, and debt management. Resources such as books, podcasts, and online forums can provide valuable insights and guidance.

By addressing these early financial considerations during residency, you can lay a solid foundation for your financial future and navigate the transition to becoming a practicing physician more smoothly.

Financial Planning for Medical Residents -Student Loan Repayment- Doing the Math

Let’s break down the process of student loan repayment for a medical resident, considering the typical financial situation and options available.

1. Assess Your Loans:

Types of Loans: Identify all the loans you have, including federal and private loans. Federal loans typically offer more flexible repayment options and forgiveness programs.

Interest Rates: Note down the interest rates for each loan. This will help prioritize which loans to pay off first.

2. Understand Repayment Options:

Standard Repayment Plan: Fixed monthly payments over 10 years.

Income-Driven Repayment Plans: These plans adjust your monthly payments based on your income, which could be beneficial during residency when income is lower.

Forbearance or Deferment: You might be eligible to temporarily postpone payments, but interest may still accrue.

3. Budgeting:

Calculate Monthly Income: Determine your monthly income after taxes and any other deductions.

Estimate Expenses: Include rent, utilities, groceries, transportation, and any other essential expenses.

Allocate for Loan Payments: Decide how much you can realistically afford to allocate towards loan payments each month.

4. Loan Repayment Strategies:

Aggressively Pay Off High-Interest Loans: If you have high-interest loans, consider paying them off more aggressively to minimize interest accrual.

Consider Income-Driven Plans: Opting for an income-driven repayment plan can lower monthly payments during residency when your income is lower.

Public Service Loan Forgiveness (PSLF): If you plan to work for a qualified employer (such as a non-profit hospital) for at least 10 years, you might be eligible for loan forgiveness under PSLF.

Example Calculation:

Let’s say you have $200,000 in student loans with an average interest rate of 6%. During residency, your income might be around $60,000 per year.

Standard Repayment: With a 10-year repayment plan, your monthly payment would be around $2,220.

Income-Driven Repayment: With an income-driven plan, your monthly payment might be significantly lower, based on your income and family size.

Tips:

Live Within Your Means: Keep expenses low during residency to free up more money for loan payments.

Emergency Fund: Build an emergency fund to cover unexpected expenses and prevent reliance on credit, which can add to your debt burden.

Stay Informed: Keep abreast of any changes to student loan policies or forgiveness programs that might benefit you.

By carefully assessing your loans, understanding repayment options, budgeting effectively, and considering strategies like income-driven repayment or loan forgiveness programs, you can navigate student loan repayment as a medical resident more effectively. Consider consulting a financial advisor for personalized guidance based on your specific situation.

Financial Planning For Medical Residents – Different Payment Options for Student Loan Debt in the U.S.

Direct Consolidation Loans, Income-Driven Repayment (IDR) plans, Public Service Loan Forgiveness (PSLF), and refinancing are all essential components of managing student loan debt in the United States.

Direct Consolidation Loans:

Direct Consolidation Loans are federal loans that allow borrowers to combine multiple federal student loans into a single loan with one monthly payment. This process simplifies repayment by combining various loans into a single loan, often extending the repayment period and reducing the monthly payment amount. However, it’s crucial to note that while consolidation can streamline repayment, it may not necessarily lower the overall interest rate or save money in the long term.

Income-Driven Repayment (IDR) Plans:

Income-driven repayment plans are designed to make student loan repayment more manageable for borrowers by tying monthly payments to their income and family size. These plans include options such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Under these plans, borrowers typically pay a percentage of their discretionary income towards their student loans, with any remaining balance forgiven after 20-25 years of qualifying payments.

Public Service Loan Forgiveness (PSLF):

Public Service Loan Forgiveness is a federal program that forgives the remaining balance on qualifying Direct Loans after borrowers have made 120 qualifying payments while working full-time for a qualifying employer, such as a government agency or non-profit organization.

PSLF provides an incentive for individuals to pursue careers in public service while also helping to manage their student loan debt burden. It’s important to note that not all federal loans or repayment plans qualify for PSLF, so borrowers should carefully review eligibility requirements before pursuing this option.

Refinancing:

Refinancing involves replacing existing student loans with a new loan, often from a private lender, with different terms, including interest rates and repayment options. Borrowers typically refinance their loans to secure a lower interest rate, reduce monthly payments, or change the repayment term.

However, refinancing federal loans with a private lender means forfeiting access to several federal benefits. These include income-driven repayment plans, loan forgiveness programs, and deferment or forbearance options. Therefore, borrowers should weigh the potential savings against the loss of federal benefits before deciding to refinance.

In summary, Direct Consolidation Loans, Income-Driven Repayment plans, Public Service Loan Forgiveness, and refinancing are all tools available to help residents manage their student loan debt effectively. Each option has its advantages and considerations, so residents need to research and carefully evaluate which options align best with their financial goals and circumstances.

Financial Planning for Medical Residents – Student Loan Repayment Strategies for Residents

Income-Driven Repayment Plans:

Opt for income-driven repayment plans like PAYE (Pay As You Earn) or REPAYE (Revised Pay As You Earn) during residency to keep monthly payments manageable based on your income.

Public Service Loan Forgiveness (PSLF):

Consider working in a non-profit or public sector job during or after residency to qualify for PSLF, which forgives the remaining loan balance after 10 years of qualifying payments.

Loan Deferment or Forbearance:

If needed, explore options for deferment or forbearance to temporarily pause payments without accruing additional interest, though this may prolong repayment.

Refinancing after Residency:

Once your income increases post-residency, explore refinancing options to potentially lower interest rates and save on the total repayment amount.

Budgeting and Financial Planning:

Develop a budget to manage expenses effectively during residency, allocating funds towards loan payments while still covering essential living costs.

Additional Income Streams:

Explore opportunities for additional income streams such as locum tenens work, teaching, or consulting to supplement your income and accelerate loan repayment.

Automatic Payments and Interest Reduction:

Enroll in automatic payments and seek out interest rate reduction programs offered by loan servicers to minimize interest costs over time.

Loan Forgiveness Programs:

Research and take advantage of any loan repayment assistance programs offered by your employer, state, or specialty organizations.

Conclusion:

In conclusion, financial planning is a critical aspect of a resident physician’s journey toward achieving financial stability and long-term success. While the demands of residency can be intense, allocating time and effort toward understanding personal finance can yield substantial benefits in the future.

By implementing the strategies outlined in this guide, resident physicians can lay a solid foundation for their financial well-being, allowing them to navigate challenges such as student debt, limited income, and uncertain career trajectories with greater confidence and resilience.

As resident physicians transition into attending roles and beyond, the principles of financial planning remain relevant and adaptable to their changing circumstances. Regularly reassessing financial goals, optimizing investment strategies, and seeking professional guidance when needed can help physicians stay on track toward achieving their desired financial outcomes.

Ultimately, by proactively managing their finances, resident physicians can not only secure their own financial future but also gain the freedom to pursue their passions, contribute to their communities, and lead fulfilling lives both personally and professionally.

FAQs

Comprehensive financial planning is a holistic approach to managing your finances. It involves evaluating your current financial situation, setting specific goals, and creating a detailed plan to achieve those goals.

Residents often face unique financial challenges such as managing student loan debt, saving for retirement, and planning for major life events like buying a home or starting a family. Comprehensive financial planning helps residents navigate these challenges and build a secure financial future.

Comprehensive financial planning covers various aspects of personal finance, including budgeting, debt management, insurance, investments, retirement planning, tax planning, and estate planning.

Residents can benefit from comprehensive financial planning by gaining clarity on their financial goals, developing strategies to achieve those goals, minimizing financial stress, and making informed decisions about their money.

Residents can seek assistance from financial advisors, certified financial planners (CFPs), or other professionals specializing in personal finance. These experts can provide personalized guidance tailored to the resident’s unique financial situation and goals.

References

https://www.laurelroad.com/healthcare-banking/financial-guide-for-surviving-residency/

https://wealthkeel.com/blog/financial-planning-for-a-medical-resident/